On Monday, the Governor announced that some state agencies will have to reduce their budgets by 7.5 percent next year to make way for a projected budget gap in the FY 2013-14 budget that begins on July 1, 2013. Left untouched by the budget cuts are the school-aid formula, corrections programs, the legislative and judicial branches, Medicaid, and other health-related social services.

According to the WV Budget Office, the state faces a budget gap of $389 million in FY 2014. The 7.5 percent in cuts to some agencies will reduce this gap by $85 million, or close to 2 percent of the projected FY2014 budget, while surplus lottery ($81 million) and general revenue ($87 million) will reduce the gap by another $169 million. This leaves about $135 million in revenue or cuts that will need to be filled (assuming the projections included in last year’s budget are correct) in order to balance the budget.

According to Governor Tomblin, the cuts are necessary because of anticipated increases in Medicaid expenditures and declining severance tax and lottery revenues. What was not mentioned by the Governor or the media (see here and here) was the erosion of the corporate tax base, which is the result of cuts to the corporate net income tax and the business franchise tax. There was also no mention of the reduction and future elimination of the sales tax on food. Neither of these tax cuts – not to mention dozens of other tax credits and exemptions passed over the years – were paid for with other revenue. This means that the state has drastically reduced the revenue it needs to meet its budget priorities.

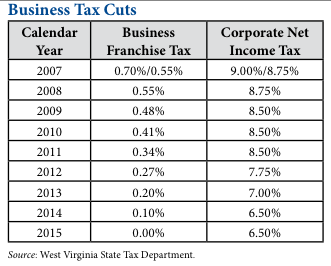

To get a better idea of what I am talking about, let’s look at how the business tax base has shrunk over the last few years. Beginning in 2007, the state began reducing its corporate net income and the business franchise tax rate. Between 2007 and 2013, the corporate net income tax will be reduced from 9 to 7 percent and the business franchise tax will be reduced from 0.7 percent to 0.2 percent (see table below). Eventually the business franchise tax will be eliminated and the corporate net income tax will fall to 6.5 percent.

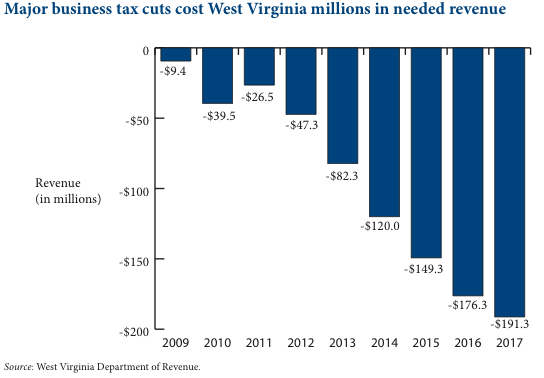

Because of these rate reductions to the state’s two main business taxes, it has reduced business tax revenue dramatically. According to the WV State Tax Department, these tax cuts will reduce revenue by $82 million in 2013 and $120 million in 2014. Once all the cuts are fully implemented, it will reduce revenue by close to $200 million (see chart below) per year.

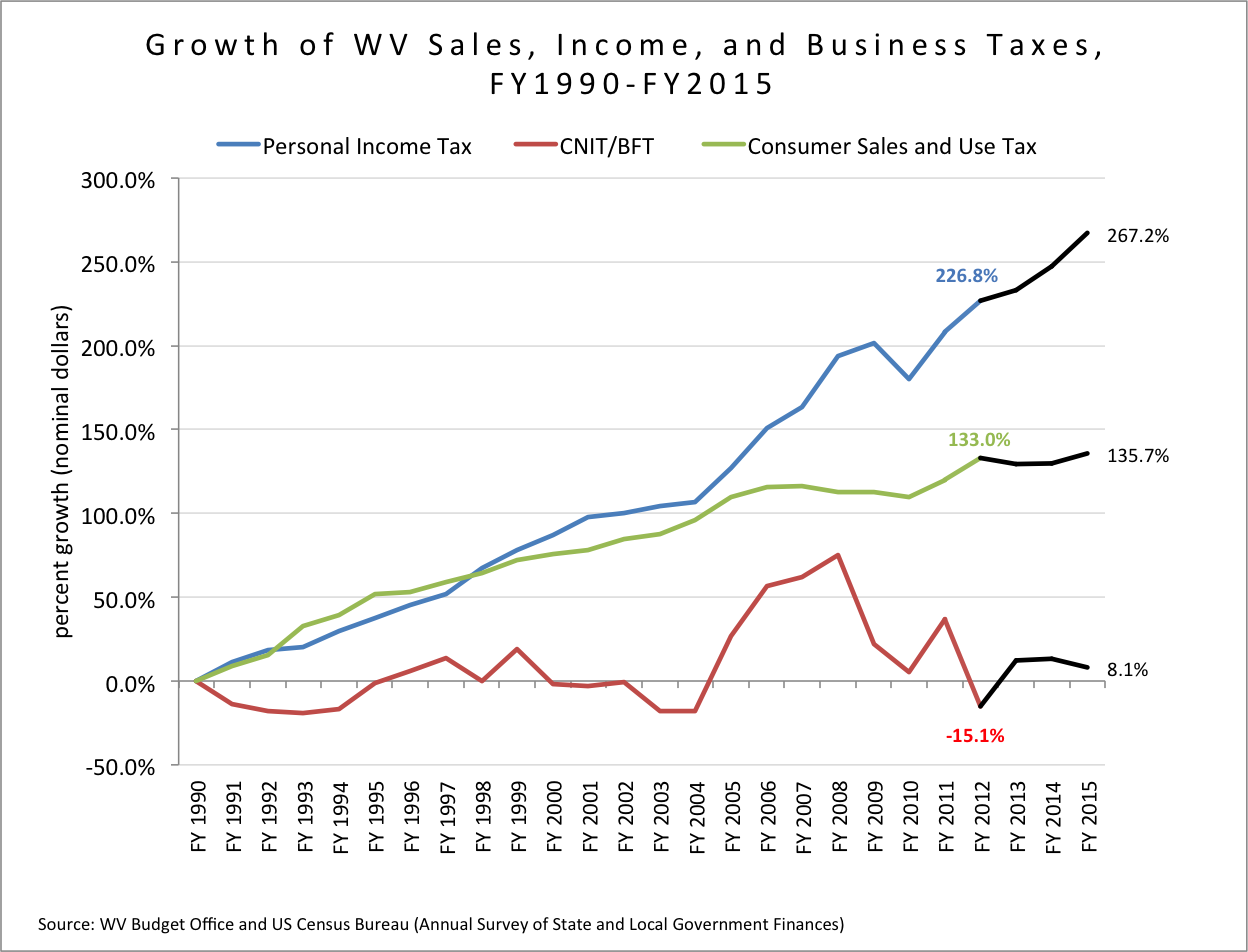

Another way to put these corporate tax cuts in perspective is by comparing the growth in corporate taxes with the growth in sales and personal income taxes over the last two decades. While personal and sales and use taxes have more than doubled from FY1990 to FY2012, the corporate net income and business franchise tax has shrunk by 15 percent. (Some of the early decline in business taxes in the early 1990s was because the state enacted “super tax credits” in the mid-1980s that depressed the growth of the tax. Many of these credits where eventually phased out.) Notice that the recent decline in business tax growth began in FY2008, the same time as the business tax cuts were being phased in (see table above and chart below).

In fact, the state collected $188 million in revenue from business taxes in FY2012 compared to $222 million in FY1990, two decades ago. From 2008 to 2012, business tax collections have declined by $100 million while sales tax collections have grown by $106 million and personal income taxes by $170 million. (One reason for the slow growth of the sales tax is the reduction in the food tax, more on that below).

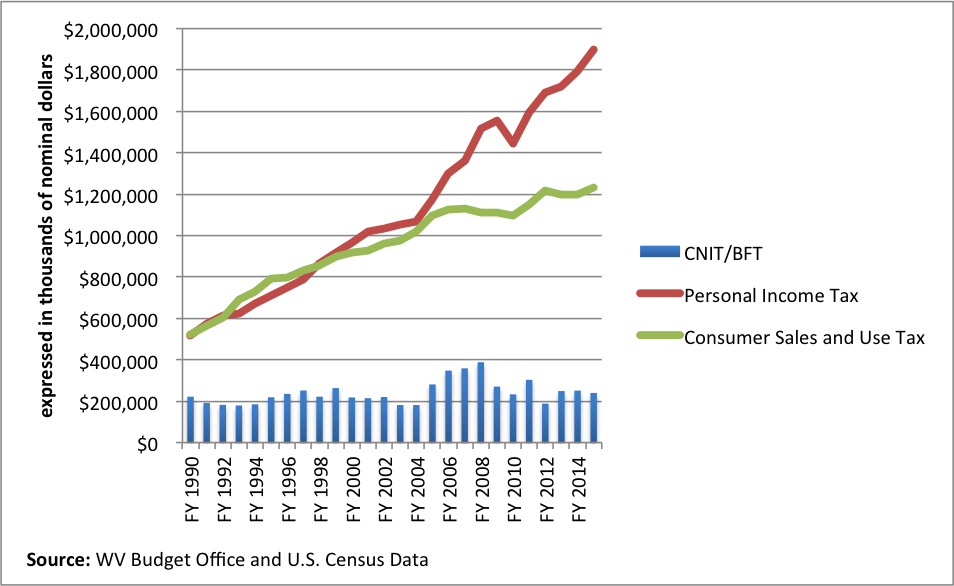

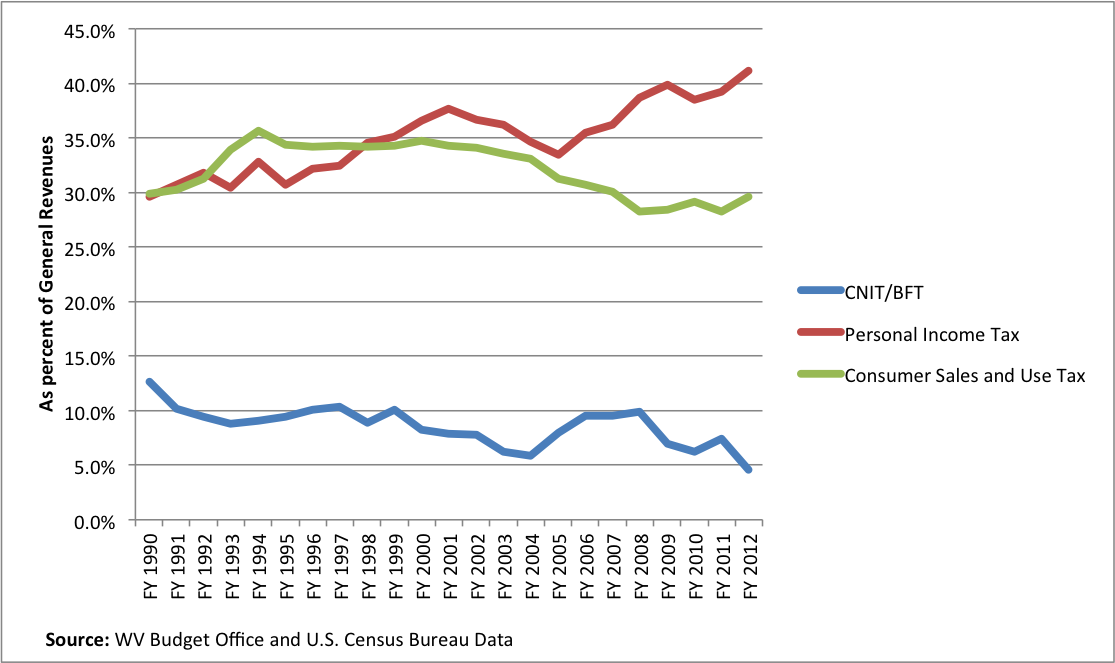

The declining business tax base can also be examined by looking at its share of general revenue collections. In FY1990 the corporate net income and business franchise tax comprised about 13 percent of general revenue tax collections compared to just under 5 percent today. In 2008, it made up just under 10 percent. Meanwhile, the sales tax has also shrunk as a share of general revenues (see chart below).

While there are many factors that have led to the decline in business taxes as a share of the budget – including recent growth in severances tax collections – the fact remains that the business tax base has shrunk dramatically over the past few years. No matter how you slice it – whether comparing it to the growth of other taxes, actual revenues, or as a share of the budget – business tax collections are becoming a smaller part of the revenue our state needs to fund important programs and services.

The reduction in the sales tax on food – whether you are for or against it – has also played a role in our budget gap because the state never replaced the lost revenue. Since 2006, the state has been gradually reducing the tax from 6 percent and it is scheduled to be eliminated by July of 2013. According to WV Tax Department, every 1 percent drop in the tax rate results in $26 million in lost general revenue. This means that it will reduce our sales tax revenue by an estimated $156 million in FY2014. While taxing food is a very regressive tax on low-income families, the revenue should have been replaced if we want to balance our budget.

Over the last decade the state also lost revenue from not decoupling from federal tax changes. For example, in 2000 the state collected $21 million from the estate tax. Now the state collects zero revenue from the estate tax because it did not decouple like so many other states did ten years ago.

As Paul Krugman often quips, we are beginning to become the Cassandra of WV budget issues. Over the past couple of years, we have warned policymakers and others about the ramifications of cutting taxes without replacing the revenue. (see here, here, here, here, here, here, here, and here). In fact, in one of our very first reports in 2008 on the cuts to business taxes we concluded:

Last year, significant reductions were made to the business franchise tax without replacing the revenue lost to the General Revenue Fund, and the same course of action is being pursued today. The additional cuts in business taxes embodied in SB 465 and SB 680 threaten to significantly undermine the ability of the state toprovide quality public services. Some combination of a sharp drawing-down of the states reserves, reductions in state services, and increases in other taxes seems almost inevitable during the next decade.

In acting upon SB 465 and SB 680, it is important for policy makers to consider the fiscal implications not just on a short-term basis but also for the long term. It is in the “out” years that state policymakers will have to make some difficult choices concerning whether to raise taxes or cut government services. . In the end, policymakers should balance the short-term marginal effects of cutting taxes for businesses against the long-term benefits of investing in quality public structure.

As we pointed out four years ago, there is no such thing as a free lunch. If you want tax cuts, you need to pay for them. There is no voodoo economics, tax cuts do not pay for themselves. Unlike the federal government that can run deficits, the state must rely on the revenue it receives each year to make the important investments we need to make West Virginia a better place to raise a family and conduct business. When you deprive the state of revenue – like depriving you car of gas – it cannot run effectively and the places you want to go become further and further out of reach.